A few days ago I discussed the coin toss game ‘triple or bust‘. The game is between Alice and Bob. Alice start the game by writing a $ 1.00 IOU to Bob. Alice then makes at least six subsequent tosses with a fair coin. On each ‘heads’ Alice triples the IOU amount. On ‘tails’ she sets the IOU to zero.

The question is: how much should Bob be prepared to pay Alice to participate in this game?

As Bob can repeat this game as often as he likes, he focuses on the gains to be obtained in the long run. These are given by the expectation value for this game, which are easy to calculate. The game starts with an IOU dollar value of 1.00. On each coin toss the average IOU increases to 3/2 times the amount before the toss. That means that after the nth coin toss, the expectation value for the IOU is (3/2)n. Alice can prevent this value to grow out of control by stopping at n=6 (completing six tosses). This sets the expectation value for the game at $ 11.39.

However, one might also reason as follows: in each game Alice can continue the tossing until tails shows. This voids the IOU and Bob will walk away empty handed. The game is worthless to Bob.

How to reconcile both reasonings?

The key issue is: what do we mean by the phrase “in the long run”? How many repeat games are required to achieve a gain per game that is close to the expectation value? The chances for Bob to win a game of n tosses is 1 out of 2n. To reach the expectation value, N the number of repeats of the game, needs to be large enough to yield a number of wins much larger than 1. This means N >> 2n.

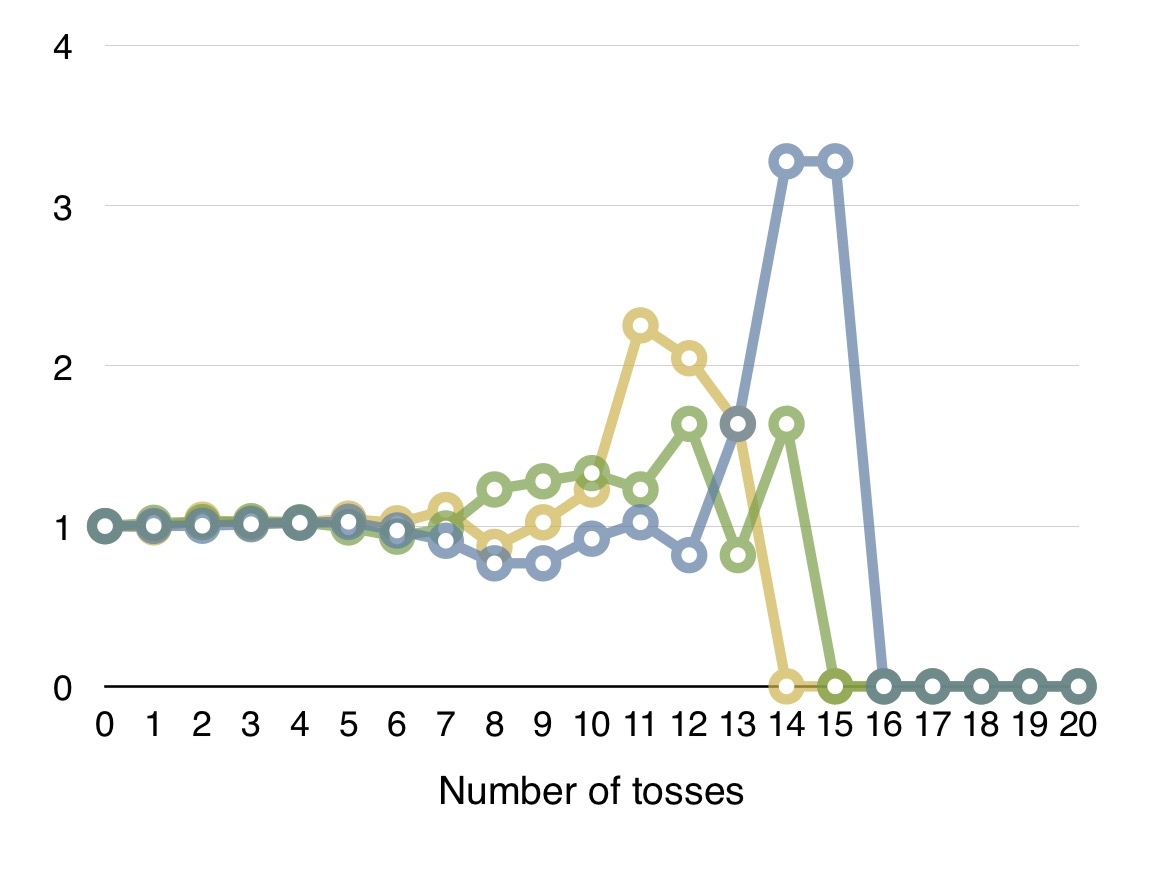

Let’s tell Alice to make exactly n tosses per game, and see how Bob fares for a given number of repeats of the game. Suppose Bob has enough time to spare to reach N = 10000. For this N value, at around n = 13.3 we have 2nequal in magnitude to N. So for n, the number of tosses per game, significantly smaller than 13 (N >> 2n) Bob can expect to walk away with close to 1.5n dollars per game. For n reaching values close to 13 or 14, it is completely uncertain if Bob will win a game. Effectively, after 10000 repeat games, Bob’s total return takes the shape of a lottery ticket. For n much large than 14 (N << 2n) Bob has vanishing odds to reach a win.

The above plot shows the earnings for Bob obtained in three independent runs of 10000 games each. The horizontal axis shows n the number of coin tosses per game. The vertical axis shows Bob’s earnings per game divided by the expectation value 1.5n. In line with the reasoning above, Bob’s earnings follow the expectation value. Around n = 14 the fluctuations in his earnings become large, and a transition happens. Above n = 14 Bob becomes progressively unlikely to make any earnings. If Alice has full freedom in increasing n, Bob is guaranteed to walk away empty handed.

In essence, the cause for the expectation value failing to represent the earnings of a participant to this game is the skeweness of the payout distribution increasing without bound. Mathematically the expected earnings for this game become ill-defined because taking the limit of N going to infinity (calculating the expectation value) followed by taking the limit of n going to infinity (allowing Alice an unlimited number of tosses) gives a different evaluation from the one based on reversing these two limits.

The same phenomenon of unbounded skeweness in the payout distribution causes the expectation values of the well known Saint Petersburg paradox to misrepresent the likely earnings.

--- this article also appeared on hammockphysicist.wordpress.com ---

Comments